Exploring the Future of LatAm VC: Predictions and Outlook for 2023

Written by Luis Arbulú, Partner of Salkantay Ventures.

It’s that time of the year: prediction time! Furthermore, given that COVID has finally hit home after almost 3 years of dodging it, I’m stuck at home instead of enjoying the slopes in Tahoe, as originally planned. Thankfully, we have a new family member to keep us occupied… meet Nube!

2022 was a very interesting year for Venture Capital in LatAm: the first two quarters continued the momentum from the record-breaking pace of 2021 in terms of capital invested, resulting in the 2nd highest annual total ever. However, after 4 (and, once Q4 numbers come out, most likely 5) quarters of consecutive decline in activity, we’re starting to settle into the “new normal” of VC in LatAm (which ironically, looks very much like the old pre-pandemic normal).

Beyond the clichéd “it’s a great time to build” and “great companies get built in times of crisis”, the contraction in funding will bring some hard choices for both founders and VCs. Venture investing is a key ingredient in the innovation ecosystem, and one that depends on many actors. In order to prepare for 2023, these are some of the key assumptions we’re using, and how we got to them.

1- The total invested in LatAm for 2023 will be between $4B and $6B (using LAVCA as benchmark)

There are two ways to reach that number… I’ll go into detail because it’s the same methodology companies should use to forecast sales, which determines everything from your marketing budget to the size of your client operations, to your milestones for the next round (also, this was my first job at Google).

Top down: trend

There are two ways you can model here. In the long (20 quarters) and excluding the 2021 bump, the level fluctuates around a pretty stable mean of $1.2B per quarter. Not only that, the “Seed-Early” number is very close to $0.5B. Late stage has been more variable (driven by a few mega-deals here and there) but it averages to $0.9B. This would give a total of $1.4B per quarter, or $5.6B per year.

Using a short-term trend, starting from Q3–2021, the quarterly total has decreased from $5.2B to $1.2B. Even though the decrease in Q3–2022 was the fastest (50% vs Q2) I’ve chosen to fit a decay function, rather than an exponential decline — there is plenty of discretion in forecasting. This would give between $1.4 and $1.0 over the next four quarters, for a total of $4.6B for the year 2023.

Bottoms up: build-up

The key assumption is that VC in LatAm is supply-constrained… the need for investment in innovation in the region is enormous and if more were available, there would be plenty of opportunities to allocate it (as it was in 2021).

VC funds typically have the same structure: a 10-year fund with an investment period for 1st checks, one for follow-ons, and one for liquidating positions (they overlap). The percentage of 1st checks and follow-ons varies by fund, but it tends to average around 50–50% (small seed funds tend to invest all on 1st checks, but they are very small for the overall analysis).

Considering ~$8.5B has been raised by VCs in the past 6 years, and $5B in the past two (and assuming $2B is raised in 2023 — this one is a big question mark given the LP market), I get $2.0B invested by LatAm VCs in 2023. Of course, not only LatAm VCs invest in the region; there are global funds active in the region (e.g. Foundation, QED, GSV, etc.), hedge and PE funds (Tiger, General Atlantic, Advent), Corporate VCs, and angels. This second group is harder to forecast (in sales forecasting you would give this a more speculative chance), but in 2021 this is what drove the massive increase and the decline in 2022.

What is the ratio of all-others:local-VCs? It’s hard to tell if there’s any correlation (more capital overall), causation (more local VC de-risks deals for outside investors) or pure coincidence. What I’ve found is that the ratio goes from 1:1 to 2:1. This would put the total for 2023 between $4B and $6B.

These two exercises give us a range. Of course, the final number can be lower or higher, but for planning purposes this has a high degree of confidence.

2- Wave of consolidations by Q4–2023: In Q4 we’ll see 2 mega-rounds for category winners and 2 less-than-overwhelming exits

When the realization of the slowdown became widespread in Q2 of this year, the common prescription was “make sure you have runway to last at least 18–24 months”, meaning that a lot of startups will be coming to fundraise in the last quarter of 2023. The hope is that the market would have recovered by then and startups would have an easier time raising at higher valuations. Companies have had to make adjustments, reduce workforce, close operation, and focus on the lines of business that will justify the lofty valuations VCs placed on them in 2021.

With the cost of capital no longer at near zero and tighter markets (see section 1), once the wave of follow-on rounds comes, we’ll start seeing a bifurcation in the later stage between those that adjusted and thrived in the new market and those who thrived only because of the capital. Venture is not a democratic asset class: “feed your winners, starve your losers” is a commonly used refrain… Those companies that used these months wisely and whose businesses are thriving with less capital, will come out stronger and see more investor interest — after all, all that fresh powder has to go somewhere; and they will be rewarded with a large round to lead a consolidation play. The other set of companies will face a very different scenario.

After 18 months of insider bridge rounds, extensions, RIFs, etc, investors in middling companies will have to make a big decision: continue funding the company without a clear path to a big, or explore a sale (maybe to one of the companies that received the mega round), or cut losses. Not only that, founders are exhausted after the whiplash from go-go-go to cut-cut-cut and SHOULD look to park the business in a better situation, rather than keep going at all costs. As a 2X founder there is one thing that always rang true to me: growth makes your job x10 more rewarding.

Sectors especially ripe for this consolidation are the following:

- Fintech (especially consumer neo-banks): balance sheets matter, bundling

- Local commerce (warehousing, delivery, etc.): economies of scale in a brutal, low margin business

- Proptech (particularly i-buyers): high interest rates and real-estate slowdown

- B2B services (SaaS, HR tech, etc.): importance of channel and impact of up/cross-selling

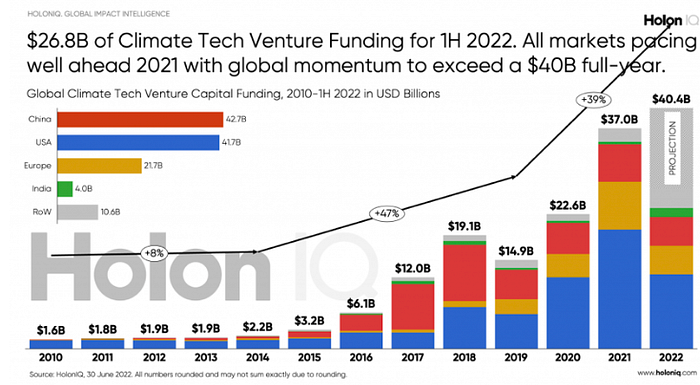

3- Climate investment: climate innovation will be a core thesis of at least 5 new VC funds

Climate tech has been the fastest growing sector in venture. Given the urgency of finding solutions, global asset managers, governments, institutional investors, DFCs, etc, are allocating more capital to finding technological solutions to climate change. Entrepreneurs and VCs are seeing this as a wide open opportunity to build multi-billion dollar companies. New climate-focused funds are getting started (i.e. Lowercarbon, 2150, TPG Rise Climate) and more large funds are dedicating a significant portion of capital to climate (i.e. Bessemer, General Catalyst, USV).

LatAm could play a key role in this industry. Although historically it hasn’t had a strong culture of research and development in labs and universities, it is home to the largest reserves of carbon and biodiversity, it has an economy closely linked to natural resources and climate activity, and is part of the global trade, which is increasingly looking at climate as a factor. Furthermore, with the increasingly integrated carbon markets, LatAm climate tech companies can become global faster.

At Salkantay we just led our third climate tech investment; Dalus Capital has been a leader in this space for a while; and Agtech-focused funds are increasingly investing in climatetech (Yield Lab, SP Ventures, Acre, etc.). Whether driven by the opportunity or by LPs, I would expect at least 5 major (>$50M AUM) LatAm VC funds to publicly announce Climate as a investment vertical.

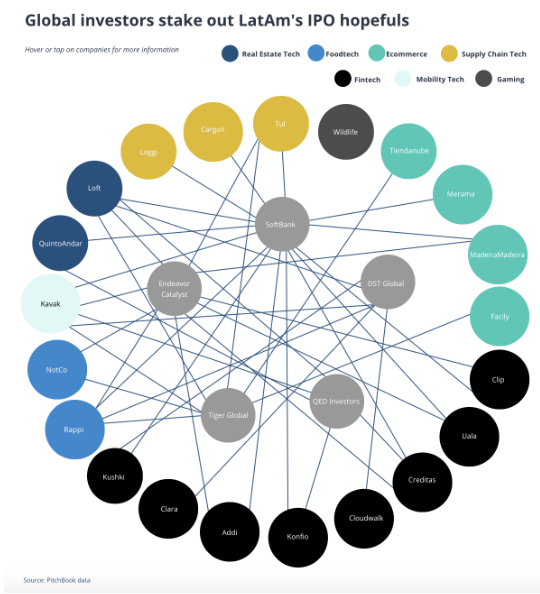

4- Exits: the public markets will stay closed for LatAm startups for a while… no IPOs* in 2022

(*) = of over $50m

2022 was completely shut down for tech IPOs globally, let alone for LatAm: after a wave of IPOs, SPACs, etc., deal proceeds plummeted 94% in 2022, with no single tech deal raising $1B (15 IPOs raised at least that much in 2021).

In LatAm, there was a pipeline of at least 20 startups looking to go public in 2022, several of which actually went through the registration process — none of them actually went through with the process, choosing to delay until the markets were more receptive. The problem is that after the dismal performance of 2021’s IPO class and overall market conditions, the expectation is that the IPO window will not reopen for at least 3 more quarters and longer for emerging market tech companies.

Coincidentally, as I was writing this, Merqueo announced this week that it had filed for IPO papers. Of course, a lot of things that can happen from registration to actually going public.

These are just some of the inputs we are using on our decision modeling for 2023. The impact will be seen in some of our strategy shifts for the next year (will be subject of another post), some of which are:

- Concentrating investments: Less deals / bigger checks

- Sector selection: doubling down on climatetech

- Pricing of deals: pre-COVID benchmarks

- Follow-ons: look at sector consolidation for scenario planning

What strategic decisions are you making for your company in 2023, and what are the driving assumptions in your model?